Commentary

April 2023 Outlook: What the banking turmoil means for the investment outlook

April 20, 2023

Averting crisis, but anxious about credit.

The US Federal Reserve (Fed) and Bank of Canada (BoC) have raised their overnight rates at the fastest pace since the 1980s. As we passed the one-year mark since the start of this rate hiking cycle, the economy and financial system appeared stable and even resilient, and markets bore the scars as higher rates led to declines in valuation multiples throughout 2022. While there have been some signs of strain, such as UK pensions, the Bank of England’s (BOE) rapid response curtailed negative outcomes. Additionally, the collapse of cryptocurrency exchange, FTX, was less related to interest rates than fraud. However, this past month’s failure of three banks: Silicon Valley Bank (SVB) and Signature Bank in the US, followed by Switzerland’s Credit Suisse being forced into a merger with its long-time domestic rival, UBS, marked somewhat of a turning point.

In comparison to prior crises, today we are at a better starting point. Issues with US regional banks are not the same as during the Great Financial Crisis (GFC), when banks held assets that were complex, massive, interlinked and then severely impaired. The legacy of those problems was a shift to tough regulatory requirements for large global banks. They now have deeper capital bases that can better withstand inevitable recession-induced asset write-downs. However, recent instability is reminiscent of more classic problems, such as outflows of deposits from banks when the rates paid do not rise in line with policy rates, combined with an inverted yield curve that impacts bank margins.

Over the weeks surrounding the stresses on the US regional banks, data releases showed depositors moved more than US$400 billion out of bank deposits (see Chart 1), with two-thirds of the outflows coming from small and mid-sized banks. Most of those flows went into financial assets that now yield higher returns than bank accounts (see Chart 2), notably money market funds. This outflow of deposits is forcing banks to sell assets and recognize losses in bond holdings due to the rise in interest rates. The Fed has taken steps to prevent the situation from worsening. Banks are now borrowing at the Fed’s discount window or using the newly established Bank Term Funding Program that was created to provide banks with a liquidity backstop. Although the rate of borrowing at the discount window remains elevated, the exodus of bank deposits slowed by the end of March and the problems have become less acute. This turmoil will require banks to bolster deposits. One way to do that is to raise interest paid on deposits, which may result in a higher cost of funding and pressure on profitability.

Chart 1: Deposits have been leaving banks at a rapid clip

Source: Federal Reserve, Macrobond

Chart 2: Deposit rates not keeping up with policy rates

Source: Federal Deposit Insurance Corporation, Federal Reserve, Macrobond

Following the banking instability, central banks seemed to face a choice between price stability (raising rates to combat stubbornly high inflation) or financial stability (injecting stimulus to save a precarious financial system). Separating out tools to deal with these two problems, they have continued to raise rates even in the face of the bank failures. What has made this whole situation a turning point, however, is that this turmoil has brought markets into a position where they are now working with the Fed rather than against it. The Fed has persistently stated that inflation remains high and financial conditions will need to tighten, and markets rallied and credit spreads stayed tight allowing for the economy to remain supported rather than constricted. Now, markets appear to be heeding the warning signs. Credit markets have seen decreased issuance and wider credit spreads.

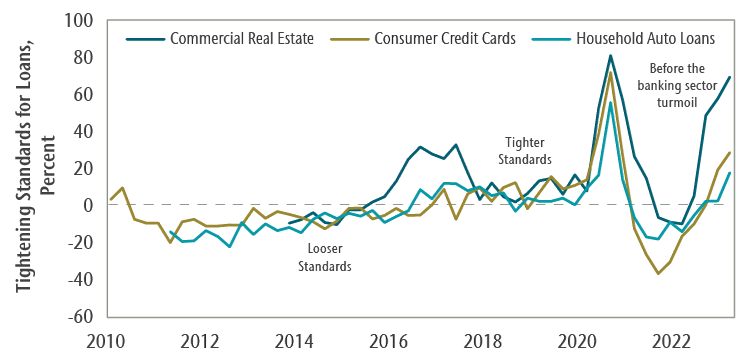

It is worth noting that a key link in the transmission of central bank actions and the economy is through bank lending. The Fed’s Senior Loan Officer Survey shows that banks have been tightening lending standards for months now (see Chart 3). Given concerns about liquidity, outflows of deposits into money market funds, costlier sourcing of funds, net interest margin pressures and weakening demand, banks are likely to pull back further on lending activity in coming quarters. This will directly dampen prospects for business investment and consumer spending to varying degrees. One sector that may be particularly impacted is commercial real estate lending. While shifting demand for office space is one factor, it is notable that smaller US regional banks with assets under US$250 billion hold about three-quarters of total commercial real estate loans. While this segment represents approximately one quarter of overall loan books, the combined supply and demand pressures imply a vulnerable sector. Overall, the message is clear: lending will be scarcer economy-wide, and an economic slowdown to recessionary levels is now looking increasingly likely.

Chart 3: Lending standards tightened to levels typically preceding recessions

Source: Federal Reserve, Macrobond

Capital Markets

Both riskier equities and safe-haven bonds have performed well over the past six months, benefiting from a sharp repricing of short-term interest rate expectations. However, this does not necessarily signal that all is well as there has been considerable volatility in the interim. Persistently high inflation led Fed Chair Powell to assert in March’s semi-annual congressional testimony that the Fed may increase the pace of rate hikes, resulting in expectations of a 50 basis-points (bps) move that pushed yields to a high of over 5% and the endpoint of rate hikes to 5.69%. After the recent bank events unfolded, expectations flipped. Two-year Treasury yields posted their single-largest, one-day drop since 1982 with Canadian yields closely following suit. For March overall, two-year yields declined by 48 bps and 10-year yields by 43 bps. This helped the FTSE Universe Bond Index rise 2.16%.

The flight to safety that was triggered by the US bank run similarly helped gold prices surge by 7.8% and silver prices by 15.2% in March. Meanwhile, energy prices declined, especially oil prices, which fell by 7% for the quarter. Natural gas prices experienced a sharp retreat, especially in Europe despite strong economic activity data and the reopening of China’s economy. The softening in energy prices was short-lived as oil rebounded within the first days of April due to OPEC’s surprising announcement of a material cut in supply.

Risk assets posted strong performance in March, with the MSCI ACWI Index up 2.5% and the S&P 500 Index closing up 3.7% in local currency terms despite regional bank stocks plunging 35.6%. Notably, even though the epicenter of the bank failure was in California’s Silicon Valley, the tech-heavy Nasdaq Index was up 9.5% in March as tech stock valuations benefited from the fall in rates. On the other hand, the S&P/TSX Composite Index was nearly flat, declining 0.2% during the month. The large weight of banks and energy in the Index was a drag on overall gains.

Portfolio Strategy

In light of the continuing effects of aggressive tightening by central banks over the past year and the recent turmoil in the US’s and Switzerland’s banking sectors, we anticipate even tighter lending standards than already posted in the second half of 2022. An economic downturn seems now more a question of “when” rather than “if”. Even as we approach the period of recession, the equity risk premium (ERP), which is the additional return demanded above lower-risk bond yields, has remained surprisingly unchanged despite recent events. While the ERP is holding in at recent average levels in Canada, it remains low in the US. As the ERP rises in response to slowing economic activity, valuation multiples will be pressured lower, compounding lower earnings. As a result, we maintain an overall underweight position in global equity markets in our balanced portfolios. We also have a modest underweight position in fixed income and are overweight in cash. In our fundamental equity portfolios, we continue to favour companies that offer stability with resilient earnings and dividend profiles.

The recent volatility in fixed-income markets has reflected a high level of uncertainty, with narratives that oscillate between expectations of further central bank rate hikes, or rate cuts mid-year. Our fixed-income portfolio decisions have been guided by valuation forecasts in line with our unwavering outlook for a mild recession, and our belief that central banks are nearing the end of their tightening cycles, although we do not foresee interest rate cuts in the near term. We remain underweight credit and have a modestly short duration position.

We anticipate that contracting lending standards will support central bankers’ goals of slowing the economy. We will closely monitor and assess the conditions around the economic slowdown to gauge what the recovery may look like and position portfolios accordingly.