Commentary

Q3 2024 Outlook: Clean and sweep

November 27, 2024

Looking at the full accumulation of outcomes from this year of elections, it has become evident that incumbents around the world have generally been routed. For the first time since World War II, every governing party up for election in a developed country lost vote share and has either been voted out of office, or in some countries been forced to work with opposing parties in a coalition. Pundits have cited a variety of reasons for this phenomenon. One explanation reaches back in time, interpreting this year’s elections as a full repudiation of the economic inequality that has bubbled since globalization. The period after the Great Financial Crisis saw populace anger slowly crescendo into the post-pandemic higher inflation period that resulted from the surge in fiscal support. Politicians likely learned that inflation is damaging to election prospects and will be more attuned to any uptick and voter dissatisfaction.

This has all come into sharp relief with the decisive outcome of a Republican sweep in the US election in early November. In contrast to the first term, this administration should be more prepared and consequently more effective, which means more of the platform being implemented. It remains to be seen, however, which of the specific tax, tariff, immigration, housing and health policies proposed through the campaign will get enacted. This is because while numerous policies have been articulated, the President-elect likes to be seen as a deal maker and is transactional, looking to drive a good bargain for the US. The upshot, therefore, is far greater uncertainty in outcomes than what markets are currently anticipating.

This backdrop is different

Financial markets have so far been applying the same reaction function from Trump’s first tumultuous term to today, which is evident in the immediate post-election surge in stocks, the US dollar and bond yields. However, this does ignore some significantly different characteristics in today’s market environment compared to the President-elect’s first term.

For one, CPI inflation in 2016 averaged about 1.5% y/y in the US, recovering from near-zero in 2015. Today, inflation has “recovered” from 4% in 2023 to 2.6% in its latest October reading. The more stable core inflation measure, that strips out the volatile components, is still above 3% with recent 3-month annualized rates now creeping higher (3.6%). This suggests a lingering stickiness in inflation that has yet to be dealt with. Planned deportations would lead to a decline in the prime-age workforce and labour supply, which is ultimately inflationary. However, dissatisfaction with high inflation contributed to voter frustration. So while US policymakers appear committed to extending tax cuts and continuing with demand side stimulus, they may be constrained from doing so because upside inflation pressures could pose a problem for mid-term elections. But more directly, the President’s nominations for Cabinet and leadership positions (including National Security Advisor and Department of Justice) are being sourced from elected officials within the House of Representatives, narrowing the majority cushion and threatening the ability to pass tax legislation in 2025. Thus, actual stimulus may be more constrained than is currently being projected by markets.

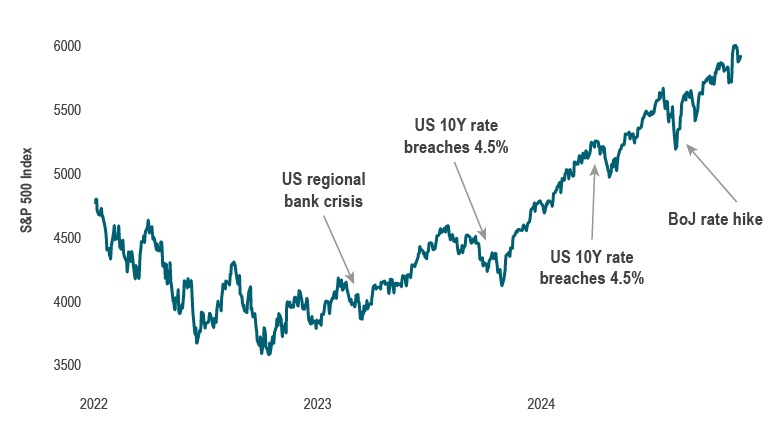

Second and relatedly, interest rates in 2016 were extremely low, hitting a then-all time low of 1.1% in July 2016, after the Brexit vote. Today, US 10-year rates are trading in a broad range of 3.75% to 4.5%, levels that harken back prior to the Great Financial Crisis. Notably, rates at this level are also associated with heightened market volatility. Over the past three years, as equity markets have risen, we have experienced four bull market selloffs. Two were sparked by events — the US regional bank crisis in March 2023, and the Bank of Japan moving its policy rates up from 0.1% in August 2024, thereby revaluing the yen carry trade. However, the other events occurred when US 10Y yields hit 4.5%, in September 2023 and April 2024 (see Chart 1). During the 2023 sell offs, there was considerable intervention required via the expansion of the Fed’s balance sheet and the shifting of US federal debt financing away from bonds, towards short term paper. Ultimately, this latter move limited longer-term bond supply and helped to lower long-term interest rates. Perversely, however, this also meant that interest expenses on the federal debt have risen as a consequence of the inverted yield curve. These material federal debt and deficit levels may lead to spikes in longer term yields as markets assess the fiscal challenge, just as they have in France and the UK this year. The bigger issue is, however, that interest rates are now hovering right around the levels that equity markets see as challenging.

Finally, another change from 2016 is the leadership in the global world order as elections caused upheaval. As the US focuses internally, there is little counterbalancing stability. Voters across Europe are also rejecting the status quo which is in contrast with 2016, when German Chancellor Angela Merkel was 11 years into a 16-year long leadership role, an offset to the shake up from the US. It has gone by with little notice, but German Chancellor Olaf Scholz’s coalition government collapsed after less than two years in office, and is set for an election in February 2025. Similarly rickety government coalition structures persist in France, following French President Macron’s defeat in the European Parliamentary Elections and a snap domestic election resulting in a hung parliament. The forthcoming changes from the US mean that, in addition to domestic leadership challenges, each country will be dealing with upending trade relationships and seeking reliable allies.

Understanding the true trends for the coming years

Today, volatility in equity markets has dampened considerably, and sentiment indicators are tilting bullish and moving higher. Actual implemented policies are only going to be known over time, but there is a lot that could upset the bull market. The desire of the incoming President to upend the main executive departments including Defense, Justice and Health with his cabinet selections suggests the unpredictable will happen. The spectrum of potential policy outcomes is as wide as it has ever been. But there are different investment time periods, one of which is the near term, where the Fed and markets are focused on short term data and whether inflation will continue to subside. Then, there is a longer term over the coming year or two, where the new administration will implement trade, fiscal and macro policies. Ultimately we believe that we are embarking on an acceleration in the already evident shift from a low growth and low interest rate post-GFC world. But volatility in rates and equities will rise under uncertain policy setting and outcomes. All of this is mixed for investors. So, we will be watching for policies that do enhance productivity, such as investment, targeted tax cuts, and deregulation that perhaps unleash some business confidence and animal spirits. Until we get that clarity in policy, much is speculation, and we remain vigilant in appraising incoming signs for these turning points over the coming cycle.

Capital markets

While there were volatile market gyrations to start the month in both August and September, market performance was strong in the third quarter. This was somewhat reversed with weakness for bonds and equities in October. Despite the Fed’s surprise 50 bps rate cut, interest rates rose steadily after that outsized cut, with surprises on growth data coming in consistently to the upside. Perhaps most notably, third quarter GDP advanced at a rapid 2.8% pace and soft sentiment data such as the ISM Services report moved back to signalling expansion. This led market participants to pare back the likelihood of more rapidfire rate cuts, and the US 10-year yield pressed up towards 4.5%.

After a 5.5% rise in the third quarter, the S&P 500 declined 1% in October. November has seen markets recoup the October loss and more, rising around 3%, with banks, consumer discretionary, industrials and energy all performing well. Following some time to absorb the implications of cabinet picks, rate sensitive sectors and pharmaceuticals have lagged the broader move. With third quarter earnings season wrapping up, both earnings and sales growth have been outperforming expectations. Earnings growth in Q3 is over 8% higher than a year ago and three-quarters of companies have exceeded estimates. Canadian equities surged 10.5% in the third quarter. In the initial post-election period, the knee jerk expectation that tariff policy would be detrimental to all but US companies led to the TSX underperforming. This was short-lived and the TSX has since rebounded, with strength in financials and tech overcoming softer energy prices and economic malaise.

Canadian bonds posted five straight months of positive gains to September, leaving the FTSE Universe Bond Index up 4.7% in Q3 before giving back 1% in October. Canadian bond yields have been on the climb since the mid-September lows, and took another step higher in the aftermath of the election with the 10-year reaching 3.35%, its highest level since July. Since then, Canadian rate moves have lagged the US. The direction is unsurprising given proposed US policies have raised expectations of a resurgence of inflation. The path has been bumpy, but Chair Powell has clearly reinforced the market’s expectation of slower rate cuts, noting there is no need to be lowering rates given the economy’s current signals on growth and inflation.

Portfolio strategy

For the past year or longer, the debate over the macro backdrop has been whether central banks will have the ability to thread the needle and produce a soft landing in the US economy, after the high inflation and high interest rates that had not been present for two decades. Last quarter, the anxiety appeared to shift away from concerns over inflation towards growth as central banks all began easing policy. However, with the year’s elections cumulating in populist votes, the question appears to be less about soft landings and instead whether a resumption of high growth and high inflation may instead take hold. This will require looser monetary and fiscal policy to act as an offset to tightening trade and immigration policies. For the short term, the positive fundamental macro backdrop in the US, with solid growth, a balanced labour market and supportive financial conditions led us to cover the equity underweight at the beginning of October in balanced funds and maintain an underweight in fixed income and overweight in cash. Fixed income portfolios continue to hold positions that benefit from a steeper yield curve. Canadian fundamental equity portfolios are adjusting positioning to benefit from onshoring and continue to look for high-quality cyclical companies such as those in industrials, financials and materials sectors. We are assessing the combination of relatively high valuations and a potential reacceleration in growth and inflation as we look ahead to the next year – and the next four years – that will no doubt be filled with surprises.

Chart 1: Equity market turbulent when yields rise

Source: S&P Global, Macrobond