Commentary

Q2 2024 Outlook: A spike in volatility during a quiet summer

August 15, 2024

This summer has been anything but calm in financial markets, despite the distractions from the Olympics and constant political headlines. Global equities have declined, with the MSCI ACWI falling 8.3% from its July 16 peak before finding a bottom in early August. The biggest price moves were seen in Asia, led by the Nikkei that fell 25% over three weeks, but other markets including South Korea and Taiwan also declined significantly. The sell off was rapid and accelerated in the wake of the July 30 Federal Open Market Committee (FOMC) decision to keep interest rates unchanged.

Three key events piled on top of each other over this period, and drove a material risk-off move across global markets. First, data releases following the FOMC decision showed evidence of a significant slowing economy. The US ISM Index dropped to its lowest level of the year at 46.8, with the employment and production components, in particular, dropping to their lows for the year. US employment also disappointed on the headline gain of 114k, but notably the unemployment rate rose to 4.3%, more than half a percent above recent lows, which is historically a signal of a recession. Second, the world’s most dovish major central bank, the Bank of Japan (BoJ), surprised markets with an interest rate increase on July 31, from 0.1% to 0.25% and slowed the pace of its bond buying by half. This narrowed the anticipated spread on Japanese and US rates as the respective central banks policies diverge. This, in turn, caused the Japanese yen to appreciate relative to the US dollar from 162 to 145. The outcome was to reverse the attractive characteristics surrounding the Japanese yen carry-trade that profits from borrowing at low Japanese rates in a cheap currency and investing in higher yielding assets in other countries. Japanese companies, many of which are global conglomerates that will be hurt by a rising yen, also saw their share prices sell off. Third, US mega cap technology companies reported generally softer earnings, and investors questioned when the mass investment into AI related technology companies would finally pay off.

The messages beneath the surface

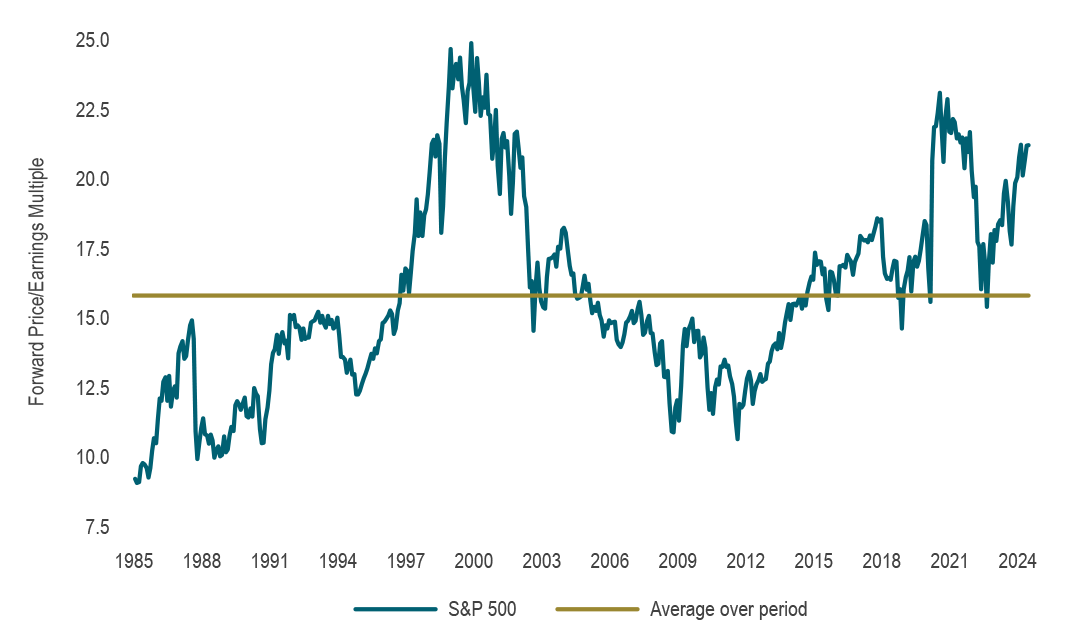

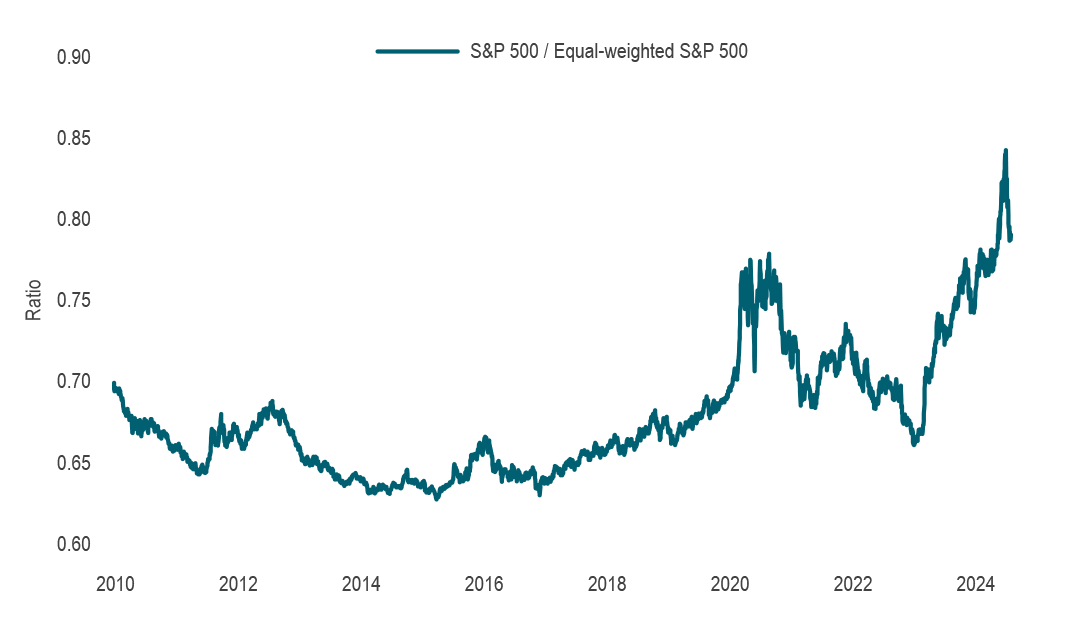

Even without the main triggers of the recent volatility, it has become evident that simply put, valuations have gotten rather expensive (see Chart 1). It is hard to see much upside to stocks overall, given they were priced for a pretty optimal scenario of decelerating inflation, steady growth and easing rates. Stocks were basically priced for a perfect outcome, with positioning consistently searching for upside and not protecting for downside. Indeed, beneath the surface, the rotation in stocks has been telling. US equities had been driven by a narrow group of stocks (Magnificent 7), that were increasingly being culled from 7 towards just 1 (Nvidia). This implied that on a capitalization-weighted basis, the gains were driven by fewer stocks, and reached a 40-year high relative to an index that weighted every stock equally (see Chart 2). However, during these past weeks, that trend began to reverse. The very expensive mega cap stocks were sold in favour of other industry groups. The broadening in leadership even saw small cap stocks outperform, at the same time as the utilities, consumer staples and real estate sectors, a highly unusual concurrence.

Chart 1: Valuations are high

Source: I/B/E/S

Source: I/B/E/S

Chart 2: Narrow leadership was over-extended Source: S&P Global, Macrobond

Source: S&P Global, Macrobond

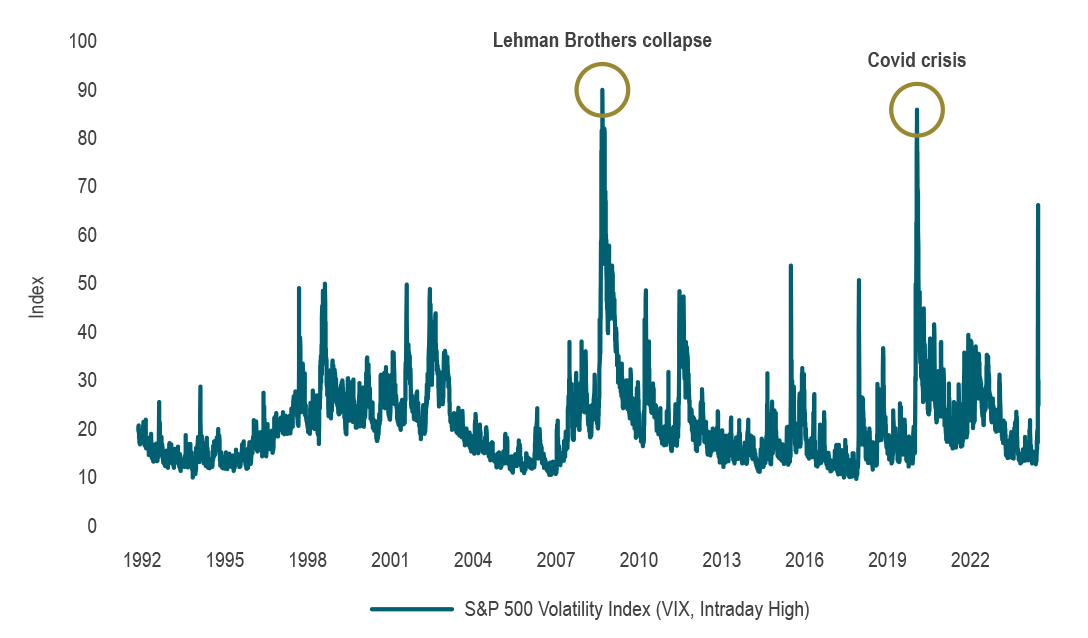

Moreover, equity market volatility spiked to an unusually high level during this period (see Chart 3). Intraday, the VIX Index jumped to its third highest level on record after the 2008 Lehman Brothers collapse and the onset of the Covid crisis in 2020. It’s especially unusual to see the surge in uncertainty, without a clear trigger event. It is also telling that gold prices actually sold off during the worst days in early August. All of this suggests that the market was experiencing a broad liquidation from extreme positioning, rather than a material risk-off event. Indeed, markets rebounded and settled down in the following few days.

Chart 3: Intraday volatility spiked to third highest level on record

Source: Chicago Board Options Exchange (CBOE), Macrobond

Source: Chicago Board Options Exchange (CBOE), Macrobond

Where are we going from here?

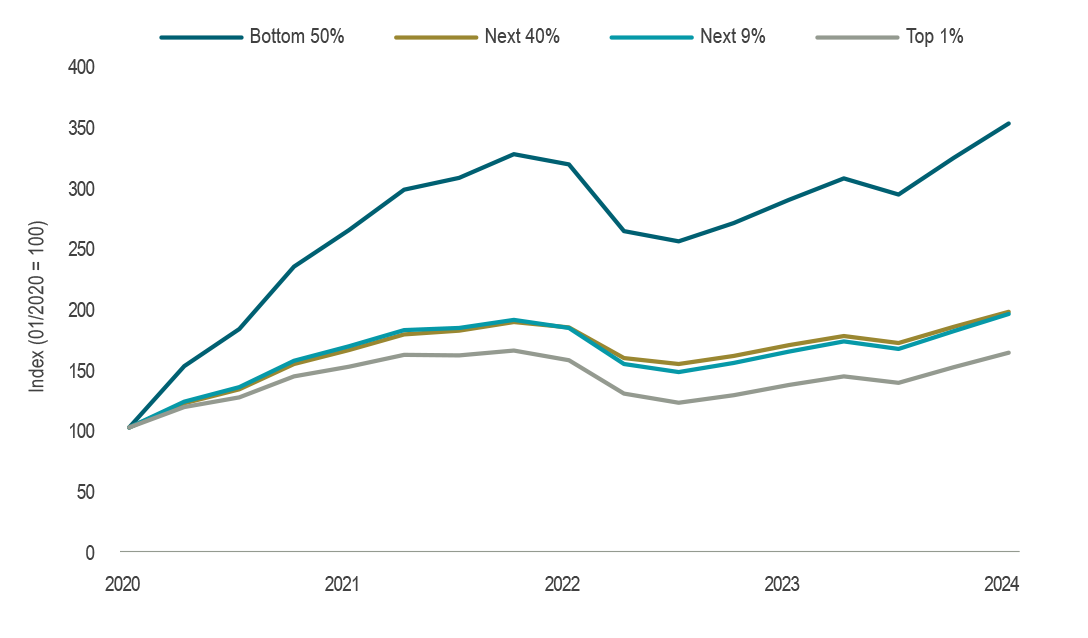

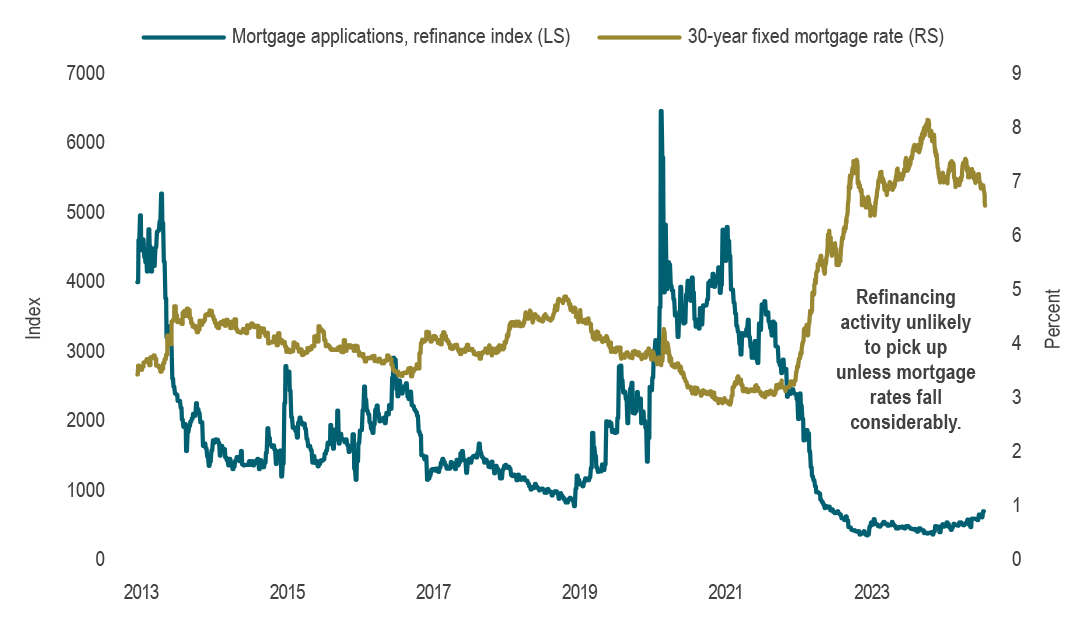

Taking stock of the recent moves and sentiment, it appears that markets are looking somewhat vulnerable at the moment. Refocusing on fundamentals, it would seem that either growth needs to rebound or risk assets will look for soothing via central bank rate cuts. Worth noting however is that any emergency inter-meeting or outsized cut would likely be interpreted poorly, as a signal that something is terribly wrong. The former growth rebound scenario may still be possible – we have been through a see-saw period of financial conditions that led to rapid responses in the economy, and this recent period has seen conditions ease. But we are cautious about the prospects for a growth resurgence at this time. Spending is critical and it typically relies on people having and keeping their jobs. The trend in employment data suggest a deterioration in labour markets is underway. But more recently, we have noted that an increasingly important factor in confidence to spend relates to the wealth effect. Indeed, since the pandemic, new households, particularly those in the lower net worth groups, have started to become shareholders, taking their stimulus cheques and putting that into stock markets (see Chart 4). The values of both stocks and homes have gone up significantly, but both are now wobbling. As rate cuts begin, this should provide some support. However, where policy easing will have the biggest support is in countries with high levels of debt held at variable rates or with high turnover of debt. That is exactly the opposite of the US, where private sector debt has largely been termed out. For instance, much of the stimulus in the US arises from the refinancing activity of mortgages when interest rates drop. However, a significant portion of American households have 30-year mortgages with effective rates in the mid-3% range. With current rates in the US around 6.75%, mortgage rates have a long way to go to even start consumer stimulus (see Chart 5).

Chart 4: Change in equity markets mattering for a growing group of US households

Equity participation by wealth distribution in the US Source: Federal Reserve, Macrobond

Source: Federal Reserve, Macrobond

Chart 5: Mortgage refinancing has flatlined Source: MBA, Bankrate, Macrobond

Source: MBA, Bankrate, Macrobond

Putting all of this together, markets are growing guarded, and becoming more attuned to a growth slowdown. Spending is becoming more cautious with less support in the US from anticipated rate cuts, all while the unemployment rate is climbing. Sentiment towards the AI boom is wavering and the last cheap place to borrow in the world has signaled the party is now over. Change is afoot in terms of market themes that have dominated in recent years, and volatility is likely to stay elevated.

Capital markets

Equity markets were broadly positive through the second quarter up until mid-July. The stability of US economic data and easing inflation supported the goldilocks outlook despite the myriad of surprising election outcomes globally, US election gyrations and escalating geopolitical tensions. Central banks began easing synchronously, with the Bank of Canada joined by the BoE, ECB and SNB. In the second quarter, the MSCI ACWI rose 4%, taking gains for the first half of the year to 15.5%. The Magnificent 7 drove the S&P 500 to all-time highs, posting a 5.4% gain in Q2 for a 19.6% first half performance, before the volatility set in through July. Second quarter earnings growth, with about 80% of companies having reported, continued at a strong pace, albeit moderating slightly from Q1. The TSX Composite lagged relative to broader equity markets, edging down 0.5% in Q2 for a more modest 6.1% gain in the first half. In mid-July, the market tone shifted and the TSX posted a 5.9% gain for the month, with a reversal in leadership notably favouring defensive sectors.

Though there has been much equity market volatility, currency and bond markets were, at least relatively, tamer. In Q2, the FTSE Canada Universe Bond Index rose 0.9%, and advanced a further 2.4% in July following the spate of weak data noted earlier. While day to day moves were generally orderly, short term interest rates in both Canada and the US dropped by nearly a full percent in the third quarter, as investors looked for safety in bonds. Credit spreads widened, alongside the risk off tone. While volatility has been evident in equities, it appears contained for now as demand for credit surfaced and issuance remained surprisingly strong through this rocky period as issuers looked to take advantage of lower rates and any positive tone. Important bond market moves included the widening in French spreads relative to other eurozone countries, given its large deficit and high government debt level drawing concerns following the outcome of the French legislative election. Commodities were broadly weaker, with declines in industrial metals, agriculture and energy.

Portfolio strategy

Confidence in a soft-landing has been high over the past year and equity markets priced in anticipation of that goldilocks scenario. This past month, a new environment has emerged. Anxiety among market participants has now shifted from inflation to growth. As a result, much of what was priced in before has been reverting, and markets are still adjusting to the changing dynamics of the yen carry trade and concern over when to expect a return from the massive investments in AI. While this anxiety persists, markets are pressuring central banks to provide stimulus, pushing short term interest rates lower. But in order to meet that demand, inflation trends need to continue declining, which is likely but not certain. Uncertainty and volatility are likely to persist over the second half of the year. As a result, we are shifting portfolio holdings towards more defensive stocks and away from cyclical stocks that are more tied to the health of the economy. For example, we are adding to utilities and consumer staples companies. Fixed income portfolios continue to hold positions that benefit when the yield curve normalizes away from inversion, while holding a modest underweight in corporate credit. Balanced portfolios remain modestly underweight equities and overweight bonds and cash, and we lean towards increasing this defensive posture if an economic downturn proves more durable. On a positive note, periods of volatility often create good opportunities, and we are on alert for stretched valuations while remaining prudent and cognizant of the growing risks.