Commentary

Forecast – 2024

January 22, 2024

This year’s Forecast examines the secular themes shaping our outlook for financial markets, as well as the shorter-term cyclical factors influencing economic growth, inflation and monetary policy. We assess market valuations and, considering all of these factors, establish our portfolio strategy framework.This year, updates to our Forecast will be featured in our quarterly Outlook publication. |

Introduction

“A short cycle and a short recession” was the dominant investment theme in our 2023 Forecast. In hindsight, our outlook and forecasts were too conservative for 2023. We had broadly expected soft economic performance in Canada, China and Europe, which largely came to pass. However, we underestimated the US economy’s resilience, specifically the impact of fiscal transfers to support consumer balance sheets, the unleashing of excess savings, as well as corporate demand for labour which kept the jobs market humming. US economic growth will end 2023 accelerating to about 2.5%. In Canada, the surge in population added to demand and aggregate economic activity (overall GDP is expected to end up about 1.2%), but disappointed on a per capita basis (see December Outlook). We expected that central banks would need to engineer a slowdown to combat inflation, ascribing about a two-thirds probability of a recession at its peak. Indeed, an upside surprise to inflation, premised on the difficulty of rebalancing exceptionally tight labour markets, was our primary risk scenario. Historically, when inflation has reached 5%, it has typically taken more than a year and an economic downturn to resolve. Last year’s recession expectation was so universal that, in the past 55 years of economic surveys by The Economist, Q4 2022’s annual US GDP forecast ranked the fourth lowest. Contrary to expectations, we were humbled by both the economy’s resilience and the slowing pace of inflation without a more material slowdown. The economy withstood the tight financial conditions, reminding us in part of the long lags associated with monetary policy but also the role that outsized policy played in supporting the economy through the pandemic.

Both stocks and bonds finished the year with material gains, recovering from a dismal 2022. The S&P/TSX Composite Index had a volatile year but ended up 11.8%. Global equities performed even better, with the MSCI ACWI Index up 18.9% for the year, led by US stocks. The S&P 500 Index gained a hefty 24% to close at 4780, exceeding our forecast of a more moderate 8% gain. We missed the mark on the massively positive investor sentiment that overwhelmingly favoured the “Magnificent Seven” (Mag 7) mega-cap stocks of Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia and Tesla, as AI moved into the mainstream, driving P/E ratios past last year’s overvalued levels. Notably, only three sectors surpassed their prior year’s valuations: information technology, telecom services and consumer discretionary. The expected outperformance of defensive stocks and corporate bonds did not materialize. The S&P/TSX, with its heavy weighting in higher dividend payers within financials, telecom and REITs broadly struggled amid higher longer-term interest rates.

Bond markets also saw large moves, but essentially did a big round trip during the year as 10-year yields in the US and Canada closed very near their opening levels. November and December were among the best months for global bonds since 2008 as tame inflation readings enabled central banks to begin to discuss the potential rate cuts. Our forecast was too conservative, calling for a return of around 2% to 5%, while the FTSE Canada Universe Bond Index ultimately closed the year up an even stronger 6.7%. Financial markets saw large moves throughout the year, responding to rapid shifts in narratives and investor sentiment and our positioning was impacted by the viewpoints. The outcome was strongly positive absolute returns for investors, and despite the miss in forecasts, many of our strategies’ overall security selection performing well.

Even as last year’s forecasts for growth turned out to be overly conservative and inflation overly worrisome, we now consider these factors for 2024. Over the next pages, we assess underlying secular themes while recognizing the cyclical influences in the foreground. We still see long-term inflation pressures, but we now note a possible resurgence in productivity that could provide some balance. In the near term, just as we began 2023 with conviction in our outlook for a recession, we begin 2024 with a strong degree of confidence that policymakers can engineer a soft-landing scenario. While many are prepared to adjust portfolios in response to a long-expected recession, (e.g., the growth side of being wrong on soft landings) it is less clear how investors will be prepared to respond if inflation is misjudged.

Chart 1: Growth has outperformed expectations

Source: Bloomberg

Chart 2: Core inflation has eased everywhere

Source: Statistics Canada, Statistics Sweden (SCB), Swiss Federal Statistical Office (Bundesamt fuer Statistik), U.K. Office for National Statistics (ONS), U.S. Bureau of Labor Statistics (BLS), Eurostat, Australian Bureau of Statistics, Macrobond

The Secular Environment

We believe the era of secular stagnation is behind us. During this period, geopolitical risks were low, and companies benefited from lower-cost alternatives through globalization and employed increasingly complex supply chains. Our secular themes indicate a shift away from an environment characterized by widespread disinflation to one where sustained inflation, more than a temporary cyclical response, challenges policymakers. However, we start our secular themes with a new development that has the potential to offset the broad inflationary pressures arising from our other secular themes.

1. Artificial Intelligence – and productivity – will reshape our world

- 2023 may come to be remembered as the year that AI entered the mainstream, particularly through generative tools based on large-language models, like DALL-E, Character AI, Bard and ChatGPT. Their widespread applicability, ease of use, and human-like interactions will facilitate adoption.

- If last year, companies were testing and brainstorming uses of AI, over the coming years companies will look to integrate it into their operations. As a result, many existing jobs will transform or even become obsolete. Research suggests AI could perform or assist with a quarter to half of current jobs. As with past technological advancements, AI is also likely to create new jobs that do not exist today.

- The ability to generate growth without inflation depends on productivity. This matters greatly, as labour markets in developed countries contract with demographic shifts. The gains from AI are expected to be swifter than those of previous technologies like PCs, the internet, mobile devices and cloud computing, which took years to reflect in official data. The effects from AI are likely to be more rapid this time – adoption will be smoothed by the human-like interface, wide applicability and attention being paid across a wide swath of industries.

- AI was a dominant market theme in 2023. Tech companies, supplying hardware, models and infrastructure and aggressively integrating AI into their operations, have been the primary beneficiaries. We will consider companies across a spectrum of adoption. Those most directly impacted will be companies involved in AI themselves, training the models and adapting them for business applications. The impact will be more pronounced in the US due to its thriving tech industry, government support and encouragement, as well as cash flow to invest. Farther down the spectrum will be businesses that enable the AI industry to thrive, through hardware manufacturing or supplying the infrastructure such as energy generation and data centers. Finally, there will be companies who will be early and willing adopters, who will benefit from margin improvement and rising revenue.

Chart 3: Most jobs evolve out of innovation

Source: The Labor Market Impacts of Technological Change: From Unbridled Enthusiasm to Qualified Optimism to Vast Uncertainty David Autor NBER Working Paper No. 30074

Chart 4: Manufacturing capex is driving business investment

Note: The ‘other’ category includes health care, educational, amusement & recreation, lodging, and religious.

Source: US Census Bureau, Macrobond, CC&L Investment Management

2. Business capital investment cycle

- Business investment was a bright spot in 2023, growing approximately 4% in the US, even amid rising interest rates. Investment in structures particularly soared, increasing by 30.3% in Q1 and as of the latest reading is up by a decade-high rate of 13.7% y/y as businesses took advantage of a range of government subsidies from the government. Fiscal stimulus moved away from consumer-targeted measures (e.g., employer tax credits, cheques, student loan deferrals, rent caps) to private sector infrastructure investment (under the Infrastructure Investment and Jobs Act (IIJA), clean energy (via the Inflation Reduction Act) and domestic high-tech manufacturing (as part of the CHIPS and Science Act).

- Public infrastructure has suffered from underinvestment, and governments have begun the renewal, with US government investment up 10% y/y to Q3 2023. The November 2021 IIJA doubled the amount of spending in a normal five-year spending plan, but these construction projects take time to implement. The spending, initiated in 2023, is expected to continue in 2024.

- Looking ahead, several factors are poised to boost capex globally. First, the urgency of transitioning to a low-carbon world is escalating. Europe will reduce its energy reliance on external sources and all countries will add to renewable (hydrogen, solar, wind) and nuclear energy sources. Commodities linked to the energy transition are likely to perform well. Second, international trade and supply chains are being realigned globally. Emerging markets (EMs) are increasingly trading bilaterally in their own currencies instead of in US dollars. The West is moving towards onshoring manufacturing, reducing dependence on Eastern sources. This deglobalization will ultimately be inflationary. Finally, the business interest in AI is enormous. Data from surveys, earnings calls, internet search terms and job postings citing AI-related skills all suggest a material planned capex likely to drive spending on machinery, equipment and intellectual property.

Chart 5: Recent fiscal bills are expected to increase deficit in coming years

Note: CHIPS and Science Act; Infrastructure Investment & Jobs Act; Inflation Reduction Act.

Positive value is deficit reducing, negative value is deficit increasing.

Source: Source: Congressional Budget Office, Macrobond, CC&L Investment Management

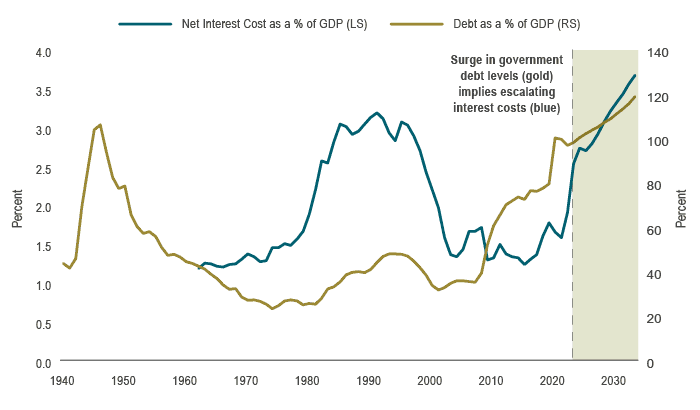

Chart 6: How high can policy rates go when there is debt to be paid?

Note: Shaded area is CBO 10-year forecast.

Source: Congressional Budget Office, Macrobond, CC&L Investment Management

3. Era of fiscal dominance

- Governments have embraced fiscal spending as a powerful crisis management tool. While that has improved economic resilience, this comes at the price of subjugating monetary policy to achieve fiscal needs, a concept known as fiscal dominance (refer to our September Outlook for more details). A notable example was the September 2022 UK budget, which triggered bond market upheaval. In response, the Bank of England initiated unlimited gilt purchases to stabilize markets and a return of inflation.

- In the US, a series of COVID-19 relief bills, financed through new borrowing without offsetting revenues, pushed the US national debt to an unprecedented $34 trillion, up from $31.4 trillion at the start of 2023. Last year’s deficit roughly doubled compared to 2022, with government spending remaining above 2019 levels, reduced tax receipts and importantly, increased interest costs for debt servicing. The $2.5 trillion annual increase in federal debt represents growth above GDP and has come at the most unnecessary time – when the economy is at period of full employment. This unsustainable development poses a risk of either higher inflation or fiscal austerity. In August, Fitch downgraded US debt from AAA to AA+, at a time when deficits are expanding due to spending, US Treasury issuance is being compounded by the Fed’s quantitative tightening (QT) and interest costs as a percentage of tax revenue are in excess of 14%, while the cost of servicing debt is rising for the first time in nearly four decades. In an effort to avoid liquidity issues, the Treasury is shifting issuance to higher-cost T-bills (over 5%), even though locking in rates for longer periods would be more cost effective.

- The likely outcome is higher neutral interest rates and increased economic and inflation volatility. Bond issuance will rise, and markets will likely raise term premiums accordingly. This is the end of the 40-year bond bull market, and the era of easy monetary policy.

The Cyclical Environment

World: Wars and elections divide, but world unites in easing policy

- The global economy defied expectations of a recession in 2023. However, the world is awash in debt, a consequence of prolonged financial repression. Policymakers aimed to moderate growth from a state of excess demand, indicating we are in the late stages of a policy-led business cycle. Without forceful policy easing to stimulative conditions, 2024 is likely to continue experiencing slowing growth. With the long lags in policy, we have yet to see the full impact of higher interest rates. Disinflation has come more rapidly across numerous countries, and has been achieved more easily than expected. Global supply shocks have eased, and combined with tighter financial conditions, have reduced inflation pressures homogeneously across the world. While services inflation remains elevated, the reduction in goods prices has done a lot of the work. In all, monetary policymakers are signaling a close to their tightening phase and are now considering when to begin bringing rates back to neutral levels.

- Geopolitics and domestic politics will be enduring and critical themes this year. Countries are engaging in wars on multiple fronts, as the unipolarity and the peace dividend from interconnected trade has fractured. Trade is increasingly focused on politically aligned or friendly countries and closer to home. This year, for example, Mexico and Canada eclipsed China as the largest source of US imports. Additionally, China’s trade with ASEAN and Latin America has soared. Notably, this year marks a record in democratic elections, with half the world’s population, representing nearly two-thirds of global GDP and 80% of the world’s equity market valuations, participating in elections. This includes nations like India, Mexico, Taiwan, the UK and the US.

- The IMF projects global growth will slow to 2.9%, below the 20-year historical average of 3.8%. EMs are expected to drive much of the growth, notably India (6%) and China (4.7%). Despite a resilient US economy, advanced economies are likely to slow further, with deleveraging taking place in heavily indebted countries.

Chart 7: Reshoring – US imports from Canada and Mexico surpassing China

Source: US Census Bureau

Canada: Recession to usher lower rates

- Like their counterparts in the US, Canadian consumers, who form the largest part of the economy, are likely to cut back over the next year. Canadians carry a high debt load relative to disposable income. Yet, the impact of high interest rates is taking time – 47% of mortgages have been reset to higher rates, with the balance expected to follow in the next two years. Debt servicing costs, however, are already back at their highest levels since 1990. Higher interest rates and some meeting of pent-up demand last year (e.g., new vehicle sales grew by 11.8% y/y in 2023), imply real household credit growth and consumer spending will contract. The severity of a consumer downturn might be softened by accumulated savings and wealth, but will also significantly depend on the resilience of labour markets. Despite high population growth enhancing labour supply (discussed in our December Outlook), balanced labour markets could begin to show strain if job creation does not keep pace with new immigrants.

- Housing markets are a wildcard. Under normal interest rate hiking cycles, the most interest rate sensitive sector would soften. However, world-leading population growth and limited housing supply should support residential demand overall (as detailed in our July Outlook). The Bank of Canada (BoC) easing should come sooner than in the US, but this could be delayed if reduced mortgage rates reignite excessive housing demand. Both our consumer and economy appear much less resilient than the US. Nevertheless, business capex, reinforced by our secular themes, should help boost productivity. Fiscal policy offers potential upside risks as the minority Liberal government could call an election within the next two years. Although a global recession may marginally reduce demand for Canadian exports, the robustness of the US economy could provide a compensatory effect.

- Headline inflation has shown significant improvement, falling from 5.9% y/y in January 2023 to 3.1% y/y by year’s end. Inflation in Canada appears more persistent than in other countries, partly owing to consistently high shelter costs (which grew by 5.9% y/y in November 2023), with both rents and mortgage interest costs continuing to pressure inflation to the upside. These factors will ultimately contribute to slowing demand and disinflation in goods and non-shelter services. However, for now, core inflation metrics remain at the high end of the BoC’s target range (core CPI 3.4% y/y), though they are showing signs of progress (2.8% on a 3-month annualized basis). This trend will be closely watched for any change in momentum.

Chart 8: 100% of of mortgages will have payments increase in the next 3 years

Source: Bank of Canada Financial System Review, 2023

Chart 9: Mortgage debt servicing costs highest on record

Source: Statistics Canada, Macrobond

US: Lower interest rate sensitivity, dampening prospects of a slowdown

- Of all the major world economies, the US is experiencing the slowest impact from policy tightening, resulting in relatively strong growth compared to other developed countries. US consumer debt is at a more manageable level than it has been in years, and households with long-term fixed rate mortgage debt have not felt the higher rates. Business borrowing has been termed out. Labour markets are more balanced, with a reduction in unfilled job openings and a persistently low unemployment rate. Low-skilled workers are seeing real income gains, while high-income consumers benefit from the wealth effect. While delayed, the prior increase in policy rates will weigh on growth this year, as evidenced by increased credit card usage and rising delinquency rates.

- Business spending and fiscal policy will likely be buoyed by the spending out of the trifecta of the IRA, Infrastructure and CHIPS bills. However, the federal deficit, now at 6.6% of GDP, remains a serious risk. Fully two-thirds of federal spending is now non-discretionary and growing due to demographic trends. Discretionary spending is unlikely to contract, particularly with the upcoming US presidential election. Historically, recessions during election years (1960, 1980, 2008, 2020) have resulted in the incumbent party losing power. Therefore, preventing a recession will be important in this high-stakes election to focus attention on the issues at hand. Despite stimulative fiscal policies and full employment, the Fed has signaled its intent to cut rates to a more neutral stance. This “pivot” – cutting rates before a significant rise in unemployment – supports a soft landing, aiming to achieve the 2% inflation target without a growth slowdown. Nonetheless, we assign a lower probability to this “goldilocks” outcome than the markets, which appeared highly convinced of this scenario at the end of last year.

- A notable inflation headline closing out last year was the six-month annualized core PCE deflator falling to around 2% in November, effectively signaling a clear path to the Fed’s target. However, if monetary and fiscal policies inject stimulus next year, in what is a fairly stable growth environment, there is a risk of an unexpected increase in growth, which may not align with continued disinflation. We believe a key underappreciated market risk is the potential for an inflation resurgence, with the Fed’s current dovish stance increasing the probability of a misstep similar to that made by Arthur Burns in the 1970s.

Chart 10: US inflation measures signaling path to Fed target

Source: BEA, Macrobond

Europe: Persistent fragility

- Europe’s growth continues to be challenged, with the Eurozone GDP ranging between 0% and 1% for 2023 and not improving much in 2024. Against the backdrop of a decelerating global economy, Europe confronted negative supply shocks last year, stemming from increased global competition in manufacturing and continued adjustments to energy insecurity. This year, Europe also faces a negative demand shock as consumers and businesses adjust to higher interest rates.

- Fiscal policy remains constrained from providing a large stimulus, although EU finance ministers did successfully put through reforms to the fiscal union at the end of 2023. These reforms will adhere to the principle of limiting budget deficits but introduce two key changes: firstly, allowing a margin of deviation depending on individual country circumstances, and secondly, aiming for a return to a deficit target of 3% of GDP over a longer period. Beyond being more realistic and achievable goals, these provide some flexibility for countries to support growth on the margin.

- Wages are a concern for all central banks. In Germany, with an unemployment rate (UR) of only 3%, labour costs (compensation per hour) are rising approximately 6% y/y, double the UR rate. Inflation has eased significantly, ending the year at 2.9% y/y, and risks are becoming more evenly distributed. Nonetheless, a slowing economy and productivity growth are expected to help control inflation in the medium term. The European Central Bank (ECB) closed out last year with a tough stance on inflation. In the coming year, the ECB’s ability to raise rates might be limited by a Fed intent on cutting rates, as any ECB hikes could lead to unwanted appreciation of the euro in an already tough international competitive environment. Rate cuts by the ECB later in the year, facilitated by a deceleration in inflation towards target, should help support a mild recovery.

Chart 11: European industrial production is stagnating

Real industrial production

Source: Statistisches Bundesamt, Istat, INSEE, Macrobond

China: Persistent structural challenges

- China’s rebound in 2023 was disappointing, largely due to weak consumer spending from a deflating property sector. To counter the slower growth and deflationary threat, policy has been easing incrementally through interest rate reductions, curbing of home buying regulations and an unusual increase in the fiscal deficit. These measures have been incremental however, as the government is wary of moral hazard and reflating the property bubble. Residential construction has slowed materially. With the maturing economy, growth is still likely to ease from last year’s rate of 5.3%.

- International trade remains a bright spot, with China diversifying trade away from the US towards EMs. China has also moved up the value chain in manufacturing, becoming the world’s largest exporter of light vehicles, and a major producer of heavy machinery poised to benefit from investment in green energy and infrastructure development. Downside risks remain, notably with worsening demographics, as India has now eclipsed China as the world’s most populous nation, as well as high unemployment rates among university-educated young workers. The ongoing property market correction has no short term fix, after significant overbuilding and the decline in confidence.

- In contrast to much of the world, China faces deflationary pressures, with a Consumer Price Index (CPI) reading of -0.5% y/y in November and producer prices falling 3% y/y. Thus, the risks are tilted towards stronger fiscal and monetary stimulus. The US-China relationship has moved to a more strategic dimension that will likely see less trade and foreign direct investment.

Chart 12: China’s trade with EM has surged compared to DM

Value of China’s exports plus imports for major trading partners on a 12-month rolling basis and indexed. EM is Brazil, Russia, India, and South Africa

Source: China General Administration of Customs, Macrobond

Valuation

VALUATIONS: Earnings growth crucial in 2024

- Canadian corporate profits peaked in early 2023, and deteriorated through the year, contracting by approximately 5% as economic momentum waned and input costs continued to rise. In contrast, US corporate profits remained stable. A solid US consumer supported by excess pandemic savings and a healthy labour market helped provide resilient economic growth.

- For 2024, we expect modest company earnings growth. Revenue headwinds remain, from slowing US nominal GDP and a likely contraction in Canada’s nominal GDP, though we expect any slowdown or recession to be relatively mild. Secular tailwinds should offset cyclical weaknesses, and operational efficiencies should, in turn, drive earnings growth. That said, we expect lackluster earnings growth in the near term, with a probable pickup in the second half of 2024.

- Profit margins contracted through 2023 but leveled off in the second half of the year, in line with our expectations. In 2024, we expect profit margins in the US and Canada to expand modestly. Companies are finding operational efficiencies, including improved inventory and supply chain management, to offset labour and other input costs. We also anticipate that input costs will be more muted in 2024 as labour markets become more balanced and wage pressures ease.

- In the US, we see a 7% rise in earnings per share (EPS) for the S&P 500 in 2024. Canada is already experiencing a more pronounced economic slowdown, and we expect 4% earnings growth for the S&P/TSX. Our 2024 EPS forecasts are $235 per share for the US and $1,475 per share for Canada, lower than consensus forecasts of US$245 and C$1,518, respectively.

- Earnings growth for MSCI ACWI is expected to land somewhere between Canada and the US. Globally, the highest earnings growth should arise from the US (outlined above) and EM, particularly India, driven by increased capital spending and exports. This growth should more than offset weaknesses in China, which continues to face secular headwinds.

Chart 13: Earnings growth to pick up in 2024

Trailing earnings growth

Source: I/B/E/S, TD Securities, Macrobond

VALUATIONS: Multiples to remain near current levels

- Valuation multiples expanded in 2023, particularly towards year-end, driven by easing inflation and economic activity, alongside the Fed’s dovish pivot that lowered bond yields. This sparked optimism for a soft economic landing, supporting valuation multiples. In 2024, price-to-earnings ratios (P/Es) in Canada and the US are likely to remain broadly unchanged at about 14x and 21x, respectively, on a trailing basis. Risks look fairly balanced. Our year-end index estimates are 4975 for the S&P 500 and 22,000 for the S&P/TSX, driven by earnings growth rather than multiple expansion. These forecasts are lower than the market’s current projections and imply mid-to-high single-digit returns in the US and Canada from year-end levels, with the S&P/TSX modestly outperforming given its lag in the recent rally.

- Global equity market valuations have also expanded. P/E multiples in regions outside of the US, such as EAFE and EM, have increased but remain below historical averages. We expect multiple expansion to be modest in 2024 for global equity markets. Regardless, we expect positive returns for global equities, and we anticipate that EM equities will outperform relative to other global regions, likely in the latter half of the year.

Chart 14: Multiple expansion limited

Source: I/B/E/S, TD Securities, Macrobond

VALUATIONS: Bonds remain fairly valued

- The outlook for bonds is more balanced. Real yields are positive compared to contained inflation expectations and central banks are likely to lower nominal yields to maintain more neutral real rates. Interest rate cuts in the first half of the year should support near-term bond returns, although these cuts are already reflected in current yields. Monetary policymakers appear to have completed their interest rate hiking cycles. As a result, the risk of pronounced negative bond returns from further interest rate increases is minimal relative to 2022 and the first three quarters of 2023. Additionally, bond investors will benefit from higher starting yields.

- The Canadian 10-year bond yield declined 0.21% in 2023 to 3.12% thanks to a year-end bond rally. We continue to believe that structural forces are likely to keep bond yields elevated relative to the post-Global Financial Crisis period. However, with our expectation of a mild recession in Canada in 2024, we believe there is room for bond yields to decline, particularly in the short-term maturities, with less opportunity for mid- and long-term yields to fall. Longer-term yields are already reflecting recession-like valuations. Additionally, technical factors in Canada, including strong demand from pension plans and an undersupply of 30-year bonds, continue to weigh on longer-term yields. However, some of these factors may dissipate as pension plans approach their target allocations and long-term bond yields become less attractive. This could result in some upward pressure on longer-term yields in 2024. For the year, we expect the 10-year Government of Canada bond yield to trade in the 2.75% to 4% range, with 2024’s starting yield already at the lower end of this range.

- The FTSE Canada Universe Bond Index rose 6.7% in 2023, narrowly avoiding a never-before-seen third consecutive year of negative returns, thanks to a strong fourth-quarter rebound. We have a positive outlook for bonds in 2024, expecting modest upward pressure on long-end yields to be offset by downward pressure on short-term yields. Credit spreads may widen in the case of a more pronounced slowdown, but given our expectations for a mild recession in Canada, spreads are likely to narrow after the initial widening. We expect a return of 3% to 6% for the FTSE Canada Universe Bond Index in 2024, compared to the current running yield of 3.94%.

Chart 15: After solid gains last year, looking for positive returns again in 2024

Source: TSX, FTSE Global Debt Capital Markets Inc, S&P Global, MSCI

Portfolio Strategy and Structure

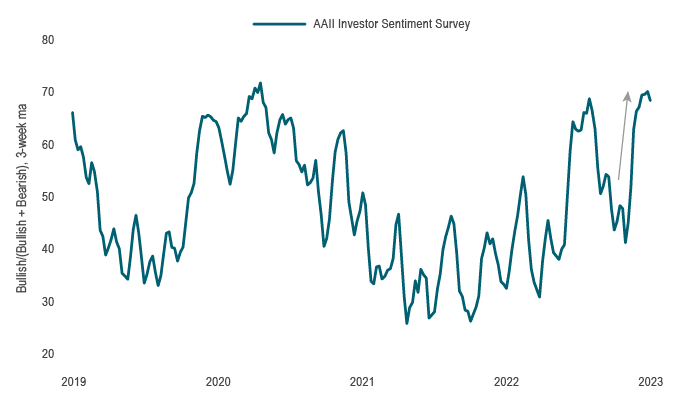

The rally across asset classes at the end of 2023 brought solid returns for investors after a dismal 2022. While much of the S&P 500’s performance throughout 2023 was attributed to the Mag 7 stocks, the broadening of the rally across all GICS sectors marked a material change in sentiment. By the end of 2023, investor sentiment, a contrarian indicator at extreme levels, moved from pessimistic to neutral, and has now reached its most bullish print since April 2021. This improvement coincided with rises in equity and bond markets. However, this now tilts risk towards the downside, particularly if the soft landing fails to materialize. Equity markets are currently “priced for perfection.” This requires validation of the aggressive rate cuts that are already priced into bond markets, continuing above-trend growth and easing inflation, a combination that seems improbable.

The Fed’s turn towards a more accommodative policy stance does bolster the soft-landing narrative for now, even if it may later be regarded as a policy mistake. Regardless, there could be some downside in equity markets if the economy slows more than expected, or if inflation deceleration stalls. Valuations, particularly in the US, have become increasingly expensive, although lower interest rates help to justify these levels. Canadian valuations are less expensive, reflecting the market’s different composition and concerns of a weaker outlook. As such, we expect equity gains to be primarily driven by earnings growth rather than multiple expansion.

Revenue growth may be challenged if nominal GDP slows materially or contracts. Additionally, given the strong performance in December and the current bullish sentiment, there could be short-term downside risk to equity market returns. Regardless, we believe that equity markets will generate positive returns overall for the year.

Regionally, we anticipate positive equity returns in both developed and emerging markets, with EMs and Canada likely to post the strongest performance overall, notwithstanding potential near-term weakness. EMs should benefit from a weaker US dollar when the Fed begins to lower interest rates. This would support economic activity in the region, as a strong US dollar negatively impacts trade volumes and a number of financial metrics, including the availability of credit and capital inflows. Canadian equities stand to benefit from an earnings recovery following a mild recession, with less risk of multiple contraction relative to the US given more attractive starting valuations.

Smaller capitalization stocks, being more sensitive to economic cycles and often exhibiting more volatile earnings than large-cap stocks, warrant a cautious view entering 2024 given the ongoing risk of a downturn, particularly in Canada. Despite the Fed’s pivot, we believe the risks associated with small-cap stocks – lower profitability prospects and increased volatility – still outweigh potential rewards. We are not forecasting broad-based multiple expansion in small caps, but remain open to increasing our exposure should signs of a broader global growth resurgence emerge.

Bond market valuations in Canada remain generally favourable, although the substantial decline in yields to close 2023 suggests overbought conditions. Regardless, with yields at attractive levels and central banks set to begin lowering interest rates in 2024, bonds present a compelling risk/reward profile.

Asset allocation

- Despite positive return expectations for both bonds and stocks, we begin the year with a defensive position. The asset mix in balanced portfolios currently favours cash due to its enhanced yield, partly a result of inverted yield curves. Both equities and bonds are underweight relative to benchmark target levels, with a smaller underweight in bonds than equities. Within equities, we have a preference for Canadian stocks over global equities.

- With equity and bond markets reflecting sizeable interest rate cuts, we should expect some reversal of the year-end 2023 rally in the near term. A market reassessment of the soft-landing narrative could trigger a selloff in equity markets that would present an attractive opportunity to rotate back into equities, and in particular, Canada, small cap, and EM.

Chart 16: Sentiment has become extremely positive

Source: AAII, Macrobond

Stock and sector selection

- While overall equity markets look expensive, certain segments have already priced in a downturn, and we are adding some early cyclical companies with favourable valuations.

- We also prefer companies capable of generating earnings growth in a weaker revenue environment. These are companies likely to benefit from topline growth due to secular trends, overcoming some of the cyclical headwinds. This includes companies that gain from decarbonization, supply chain reshoring, capital spending and construction, and those integrating or exposed to AI.

- Companies with stable and durable free cashflow are also favoured. These companies can drive earnings growth through share buybacks and accretive M&A activities (where an acquiring company’s earnings increase following a deal).

Corporate credit

- Much like equity markets, corporate credit performed well to close 2023. Yields have risen in recent years and despite tightening spreads in 2023, the all-in yield remains attractive for investors. There is strong demand in both investment-grade and high-yield credit, as they offer compelling returns compared to the ultra-low equity risk premiums that show earnings yield relative to 10-year Treasury yields hovering near its lowest level in decades.

- Corporate credit spreads, at about 155 basis points (bps) above sovereign bonds after a tightening into year-end, are around their 15-year average. These spreads are unusually tight for a period of expected weakness associated with an economic and earnings slowdown in Canada. These are far from the levels experienced in the last three recessions where spreads typically exceed 200 bps. With the year-end rally’s impact on valuations, further spread compression seems relatively limited for now.

- Credit spreads are currently in the middle of the historical ranges. We see a good degree of benefit in holding corporate bonds in areas with favourable yield carry while adjusting overall credit exposure accordingly considering the limited potential for further meaningful spread narrowing.

- Fixed-income portfolios are currently underweight in corporate credit and market weight provincial credit, relative to their benchmarks. In the near term, we expect outperformance within some of the more defensive sectors.

Chart 17: Spreads already tight leaving limited opportunity for further compression

Note: Average spread of corporate bonds in the FTSE Universe Bond Index.

Source: FTSE Global Debt Capital Markets Inc., Connor, Clark & Lunn Investment Management Ltd.

Duration and yield curve

- The fourth quarter of last year saw a drop in bond yields in the US and Canada that reversed the prior quarter’s rise. As we enter 2024, there is familiarity to the expectation for a slowdown and thus outperformance from bonds. Nonetheless, the starting point looks unfavourable following the year-end decline in yields. Adopting a long-duration strategy now hinges on a more pronounced recession given markets are pricing in five interest rate cuts in Canada starting in spring. This is an aggressive call, even with our dour view on Canada’s growth backdrop. Additionally, the market appears completely sanguine on the prospect for any reacceleration of inflation or even a growth rebound – each should increase longer-dated yields. Thus, we begin the year positioned with duration shorter than that of the benchmark.

- Our higher conviction lies in the dynamics of the yield curve. Short-term yields were pushed higher than most prognosticators thought last year, and active pension buying along with recession fears together pulled down long-term yields. This led the yield curve to reach its most inverted level since the early 1990s (about -125 bps between Canadian 2-year and 10-year yields) that stayed there for most of the year, in contrast to the rest of the world where yield curves became less inverted. In a recession, normalization led by short-term yields is likely, while the long end could see upside pressure from potential inflation or technical factors, such as global bond supply increases and continued QT, particularly in the US. Even in a recession scenario, we believe long-term rates in Canada have limited room to rally due to market pricing and technical factors that have weighed on long-end yields. Thus, we see yield curve normalization through various scenarios in 2024.

- Real return bonds also offer an attractive risk-reward profile, as the market is heavily discounting the risk of inflation reacceleration.

Chart 18: 10Y yields have retraced very quickly

Source: Macrobond

Chart 19: Yield curve to move toward normalization

Source: Macrobond

Summary

- We believe political headlines and uncertainty will dominate much of the conversation this year, muting the impact of a modest cyclical slowdown. Recent years have seen the end of secular stagnation as governments have rediscovered the power of fiscal policy, a major contributor to inflation. We anticipate continued public and private investments to strengthen supply chains, combat cybersecurity threats, fortify energy sources and business operations against climate change, and attract and retain workers through the demographic changes. Moreover, the emergence and disruption of AI has added the potential for further investment to leverage productivity gains. These themes shape our 2024 market outlook. We foresee central banks refocusing from primarily fighting inflation to a more balanced approach, considering the damage of prior rate hikes. All of this will present both challenges in the near term for corporate margins and earnings, and later opportunities as valuations become attractive. Our outlook is generally positive and we will adjust portfolio positioning to capitalize on opportunities amid the expected volatility.