Commentary

December 2023 Outlook: Our true north – strong, free…and growing

December 13, 2023

A year ago in our December 2022 Outlook, we made a case for investing in Canada. Acknowledging that, like many other countries, Canadians accumulated debt to become homeowners in the low interest rate decade prior to the pandemic, there were many positives to admire about the country’s long-term prospects. We believed that Canadian asset markets were well positioned to benefit from these positives. One of the standout reasons was the reshaping of Canada’s demographic pyramid with a large influx of new immigrants.

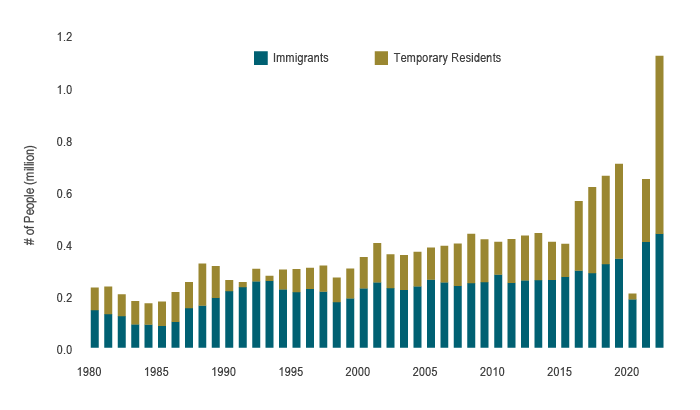

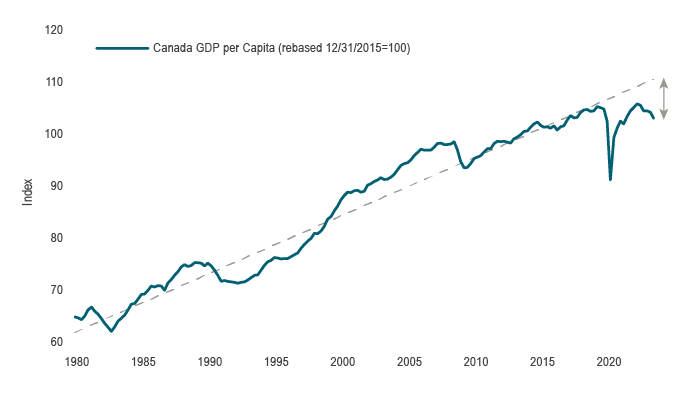

Over the past year, tightening monetary policy has produced its intended effect, and real GDP in Canada will likely grow by a modest 1.2% in 2023 according to the Bank of Canada (BoC). Economic activity is indeed softening through lower consumer spending and business investment, with both taking a hit from higher interest rates. By contrast, Canada’s population is expected to expand by nearly 3% in 2023, the strongest immigration rate in decades (see Chart 1). In total, the population will expand by more than 1 million people – net births contributing about 5%, immigration 40% and the balance non-permanent residents. Taking these together, GDP per capita has not only failed to return to its long-term trend in the post-pandemic expansion but is falling outright and opening up a material gap to our potential (see Chart 2). It is worth exploring the issue of population growth’s outsized impact on Canada, and particularly in the different ways it has been skewing data.

Chart 1: Population surging in recent years

Source: Statistics Canada, Macrobond

Chart 2: While GDP is holding in, per capita activity is falling

Source: Statistics Canada, Macrobond

Data in the context of population growth

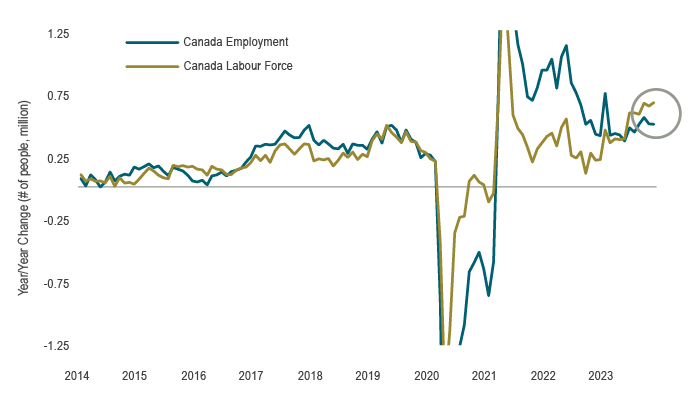

There are many reasons for the high inflation over the past few years, with services prices under particular pressure recently through rising wages. The job vacancy rates across the country more than doubled to 6% in the last year compared to the pre-pandemic period, and the influx of new workers has been a welcome source of labour supply. Today, the labour market continues to produce remarkably steady job gains, some 20 months after the start of a record fast rate hike cycle. In November, 25k net new jobs were created, a respectable gain that is above the long-term historical average and continuing a trend that saw average monthly gains of 39.1k year to date. On the flip side, Canada’s population growth casts the job gains in a different and less favourable light as the economy needs to generate a net new 56k jobs each month, in line with the labour force growth, just to prevent a rise in the unemployment rate (see Chart 3). While the data suggest still tight labour markets under normal conditions, the recent surge in population implies at best a balanced labour market today. Indeed, jobs are being filled now and job vacancy rates are now down 2 percentage points from the highs in 2022 to just 3.6% last month, the top end of the pre-pandemic range.

Chart 3: More people joining labour force than finding jobs

Note: Y-axis excludes volatile period during the pandemic.

Source: Statistics Canada, Macrobond

Across housing markets, Canada is well understood to have an affordability problem as home prices compared to incomes top global ranking tables, while home equity comprises an unusually large component of household net worth in the country. Many have attributed this issue to low housing supply. However, construction activity has actually surged in recent years with housing starts averaging some 267k over the last 3 years, 40% above the long-term average (already an achievement given the shortage of skilled trades in the sector). Even so, the new supply has not grown enough to meet the new demand and done little to alleviate the affordability issue. This is particularly true as new residents are only adding to the peak Millennial age cohort that is arriving at the prime household formation age of 32. This imbalance has left cities dealing piecemeal with trying to create supply where possible and forming more robust housing policies. As a result, this sector that is traditionally the most highly sensitive to interest rates may see very little impact through the expected slowdown.

As noted above, only about half of the newcomers are actually immigrants that stay. Understanding this difference may be important given non-permanent residents, comprised of students or those on temporary work visas, may create some further volatility in the data. This is because this group may actually exhibit pro-cyclical characteristics with the economy. For instance, should the labour market soften, workers of all types will be shed, leading many on temporary work visas to search for work elsewhere or return home. Additionally, student visas may slow as overdue government oversight will see a cracking down on sketchier educational institutions and fraud. To put it simply, a strong economy will bring new entrants, but a recession may be exacerbated If some of these new, less permanent residents choose to leave.

As mentioned above and discussed last year, there are many reasons we remain positive on the outlook for Canada. One that is very much not top of mind, but that we believe will become increasingly important, will be that the population growth will dramatically alter the demand for services beyond shelter. Governments may be forced into a renewal of spending on services, buildings and infrastructure, including hospitals, schools, roads and airports, all of which will compound other business investment over the coming years. Indeed, one of our longstanding secular themes has been the significant capex that we anticipate will evolve out of the adoption of artificial intelligence integration, green energy transformation and global supply chain reconstruction. All of this could go far in providing support to reverse what has been a dismal period of productivity.

Capital Markets

More recently, financial markets have been in a cheery mood. November was a banner month for public market assets across the board. After three straight months of negative returns in Canadian equities, the S&P/TSX Composite Index rallied 7.5% in November. That monthly gain was exceeded only five times in the post-Global Financial Crisis era. Every one of the 11 sector groups was in the black this month, led by a massive 27.4% gain in information technology. That strong gain was seen across both large and small cap stocks, with the former outperforming the latter, and cyclical sectors of the market outperforming more defensive sectors. While the November equity market gains were broad based, market breadth has been quite uneven through the year. In the US, there has rarely been a year where the strong returns were generated by so few individual stocks. The S&P 500 Index, weighted by market capitalization, has surged 20.8% year-to-date, thanks primarily to the narrow leadership of mega cap tech stocks; meanwhile the equal weighted S&P 500 Index is up by a much smaller 8.1%. Commodity prices were mixed. Notably oil prices eased back, as WTI fell 5.1% m/m to US$75/bbl and dropped further into early December. Meanwhile, precious metals prices surged to a 6-month high, rising 2.6% in the month. Gold hit an all-time high towards the end of the month, as the US dollar finally lost momentum. Following a surge off the July lows, the dollar broadly depreciated in November.

The shift in sentiment was spurred early in the month by the FOMC meeting and gained momentum with softer US CPI data in combination with Q3 GDP that was revised up to an astonishing 5.2% q/q annualized pace, more than 1.5 years after rate hikes began. This led the market narrative to shift firmly into a soft landing camp. As a result, interest rates began to reflect the likelihood that central bank rate hikes have peaked and that a slowdown is on the way. In Canada, 2-year and 10-year bond yields dropped by about 0.5% while credit spreads tightened materially despite a pickup in issuance. Combined, this led the FTSE Canada Universe Bond Index up 4.29% in November and the Long Bond Index up an astounding 8.54%. The latter marked the highest monthly return for the index since 1982. Similarly, the US Aggregate Bond Index returned 4.53%, its best monthly return since May 1985. The positive returns across both fixed income and equity markets drove traditional 60/40 balanced to post the best monthly returns since November 2020, when markets absorbed the positive COVID vaccine news. Through all that good news, one message to note is that we believe markets remain in a state of higher uncertainty and volatility.

Portfolio Strategy

Indeed, the market narrative remains in constant, rapid flux. Risk assets were displeased with higher interest rates through the summer and fall, and bond markets pushed yields higher than warranted. Once a peak in short term rates appeared at hand, interest rates have tumbled just as forcefully, shepherding in a year-end all-asset rally across public market assets. The risks from here appear to be skewed to the downside, and thus our balanced portfolios continue to underweight equities and hold cash as we anticipate earnings to come under some pressure with the slowdown in the economy. Canadian fundamental equity portfolios are selectively investing in companies with favourable valuations while maintaining a high-quality bias. Fixed income portfolios are increasingly positioning for a move toward normalization in the yield curve while remaining cautious on credit.

Much of the market direction now depends on the ability for policymakers and the economy to hit the soft landing narrative that the markets have now priced in. This in turn hinges on labour markets striking a balance from here. This is true both for the need to limit wage gains and the follow on to services prices in the CPI, and the ability for people to hold on to jobs and sustain spending. To properly assess the economic status quo of Canada, it must be acknowledged that population growth has had an outsized influence. The changing demographic profile of the country will alter short term demand dynamics for labour as well as housing. Data will appear more favourable in absolute terms, but in many ways it will be less optimistic considering the positive population shock. The influx has been beneficial from a labour supply perspective and importantly for future infrastructure development. We are optimistic about the longer run outlook for the economy, but we are expecting to see a rockier cyclical period over the next few quarters. We will explore this further in our year-ahead Forecast to be published in January. From everyone at CC&L, we thank you for your support and wish you a festive holiday season and a prosperous New Year.